.svg)

7+ Essential Accounting Tips for Small Businesses and Startups

Hey there!

You’ve decided to focus on mastering your business’s finances to ensure its success and growth.

Good for you!

Having a well-organised financial management plan will make sure you’re not wasting:

💥 Time

💥 Money

💥 Resources

By making financial mistakes or overlooking important details. Sounds like a lot, right?

Don’t worry.

Not too long ago, I was in your shoes, trying to make sense of all the financial aspects of running a business.

Today, after years of learning and experience, I’ve seen firsthand how proper financial management can make a huge difference.

But hey, I’m not here to boast about my journey. Okay, maybe a little.

But the most important reason is to show you that you can achieve financial stability and success for your business too!

Skip this guide, and you’ll miss out on how to:

✅ Keep your business and personal finances separate to stay organized and protected

✅ Leverage technology to simplify your bookkeeping and financial planning

✅ Create a budget that helps you plan for the future and avoid overspending

✅ Maintain accurate records to stay compliant and make informed decisions

Stick around as we:

Explore why managing your finances properly is crucial for your business's success.

Look at tips for using tools like Xenett to streamline your financial management.

Learn how to develop a budget and financial projections to guide your business growth.

Discuss the best practices for keeping accurate records and choosing the right accounting methods.

Now, I’m about to share what took me years to understand. And I promise it won’t be a long, boring lecture.

So grab a cup of coffee, get comfortable, and let’s get started!

Why is Proper Financial Management Crucial for Small Businesses and Startups?

Let’s talk about why managing your business's money is so important.

If you’re running a small business or startup, keeping your finances in order with accurate bookkeeping can make all the difference between success and failure.

Importance of Managing Finances Correctly

Managing your finances correctly means:

- Tracking Cash Flow: You need to know where your money is coming from and where it’s going. This helps you make sure you have enough money to pay your bills and invest in your business.

- Budgeting: Creating a budget helps you plan for future expenses and make sure you’re not spending more than you earn.

- Tax Compliance: Keeping accurate financial records makes it easier to file your taxes and avoid any penalties from the tax authorities.

- Securing Financing: If you ever need a loan or want to attract investors, having clear and accurate financial records is essential.

How Good Accounting Practices Impact Business Success and Longevity?

Here’s how:

- Preventing Cash Flow Problems:

- One of the biggest reasons businesses fail is because they run out of money. By keeping a close eye on your finances, you can avoid this problem and keep your business running smoothly.

- One of the biggest reasons businesses fail is because they run out of money. By keeping a close eye on your finances, you can avoid this problem and keep your business running smoothly.

- Informed Decision-Making:

- Having accurate financial records helps you understand how your business is doing. This information lets you make smart decisions about where to cut costs, where to invest, and how to grow your business.

- Having accurate financial records helps you understand how your business is doing. This information lets you make smart decisions about where to cut costs, where to invest, and how to grow your business.

- Building Investor Confidence:

- Investors and banks want to see that your business is in good financial shape. Good accounting practices show them that your business is well-managed and trustworthy.

- Investors and banks want to see that your business is in good financial shape. Good accounting practices show them that your business is well-managed and trustworthy.

- Planning for the Future:

- Managing your finances isn’t just about today. It’s also about making plans for tomorrow. Good financial management helps you make projections and set goals for future growth.

- Managing your finances isn’t just about today. It’s also about making plans for tomorrow. Good financial management helps you make projections and set goals for future growth.

- Avoiding Legal Issues:

- Keeping your financial records in order and complying with regulations helps you avoid legal problems that can come from financial mismanagement.

In simple terms, good financial management is like the foundation of your business. It helps you navigate through the challenges and sets you up for long-term success.

In this blog, I’ll share some easy accounting tips to help you manage your finances better and make your business stronger.

Let’s move on to the tips.

Tip #1. Mastering Financial Organization

How Can You Keep Business and Personal Finances Separate?

Hi there! Let's talk about one of the most important steps in managing your business finances: keeping your business and personal finances separate. It might sound complicated, but it’s actually quite simple and very important.

Why Open a Business Bank Account?

Opening a business bank account is the first step to keeping your finances organized. Here’s why it’s a good idea:

- Easier Expense Tracking:

When you have a separate bank account for your business, it’s much easier to see exactly where your business money is coming from and where it’s going.

This helps you keep track of all your business expenses without getting them mixed up with your personal expenses.

For example, if you buy office supplies for your business, you’ll see that expense clearly in your business account.

- Personal Liability Protection:

Keeping your business and personal finances separate can also protect you personally.

If your business runs into financial trouble, having separate accounts helps ensure that your personal money isn’t at risk.

For instance, if your business gets sued or owes money, having a separate business account can help protect your personal savings.

- Access to Business Credit:

A business bank account can also help you get credit for your business.

This means you might be able to get a business loan or a credit card that can help you manage cash flow and invest in your business.

For example, you might need a loan to buy new equipment or expand your business, and having a business bank account can make it easier to qualify for these loans.

How to Open a Business Bank Account?

- Get Your Documents Ready:

- You’ll need some basic documents to open a business bank account.

This usually includes your business registration documents and your Employer Identification Number (EIN) or Social Security Number if you’re a sole proprietor.

- Choose a Bank:

- Look for a bank that offers good terms for business accounts.

Some banks have special features like low fees, online banking, and mobile apps that can make managing your account easier.

- Open the Account:

- Visit the bank or go online to open your business account.

Make sure to set up both a checking account for daily transactions and a savings account to save for future expenses.

By keeping your business and personal finances separate, you’ll find it much easier to manage your money, protect yourself, and grow your business.

This simple step can make a big difference in your business's success.

Tip #2. Leveraging Technology for Financial Success

Should You Get Bookkeeping Software or a Bookkeeper?

Hi there! Managing your business finances can be tricky, but using the right tools can make it a lot easier. Let’s talk about whether you should use bookkeeping software or hire a bookkeeper.

What Are the Benefits of Accounting Software?

Using accounting software can bring many advantages:

Automation of Bookkeeping Processes:

Accounting software can do a lot of the work for you.

It can automatically track your income and expenses, saving you time and reducing the chances of mistakes.

For example, if you buy something for your business, the software will automatically record the expense.

Reduction of Errors:

Manual bookkeeping can lead to mistakes, especially if you’re busy or tired. Accounting software helps to reduce these errors because it handles calculations and data entry for you.

This means your records will be more accurate.

Simplification of Financial Statement Preparation:

Creating financial statements like profit and loss statements or balance sheets can be complicated.

Accounting software makes this process simple by using the data you’ve already entered to generate these reports automatically.

This helps you understand how your business is doing financially without spending hours on paperwork.

What Software Options Are Available?

There are different types of accounting software you can choose from:

Cloud-Based Solutions:

Cloud-based accounting software can be accessed from anywhere with an internet connection.

This is great if you need to check your finances while you’re on the go or if you have a team that needs access from different locations.

Examples of cloud-based software include QuickBooks Online and Xero.

ERP Systems:

ERP (Enterprise Resource Planning) systems are more advanced and can handle various business functions, not just accounting.

They’re useful for larger businesses that need to manage complex operations.

ERP systems integrate everything into one platform, from accounting to inventory management.

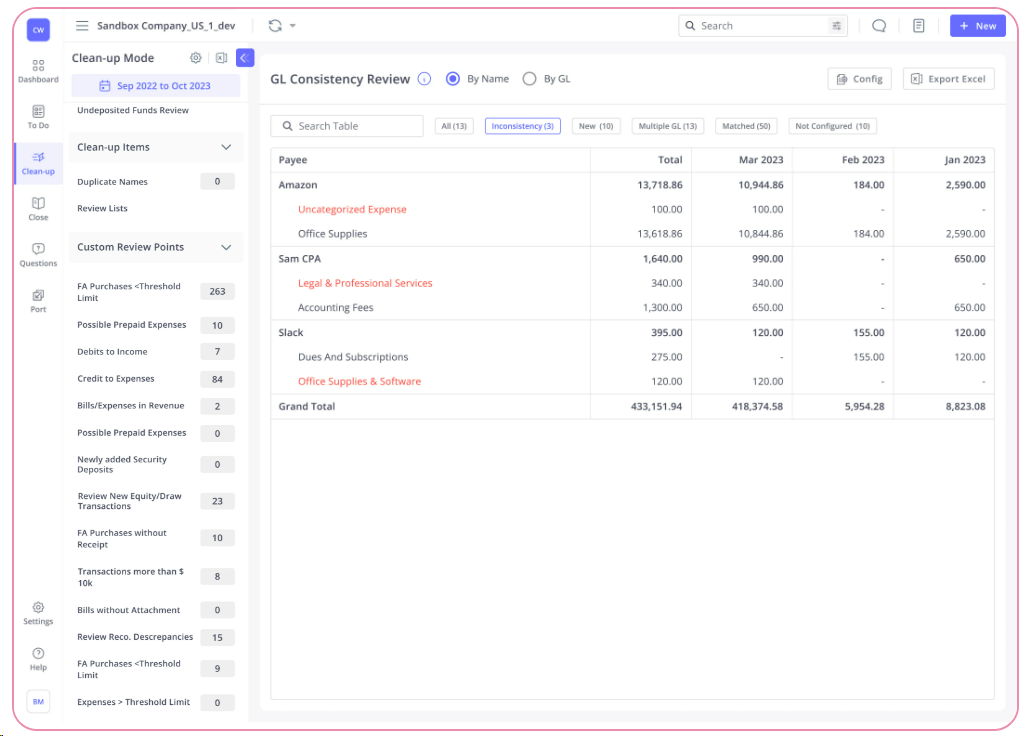

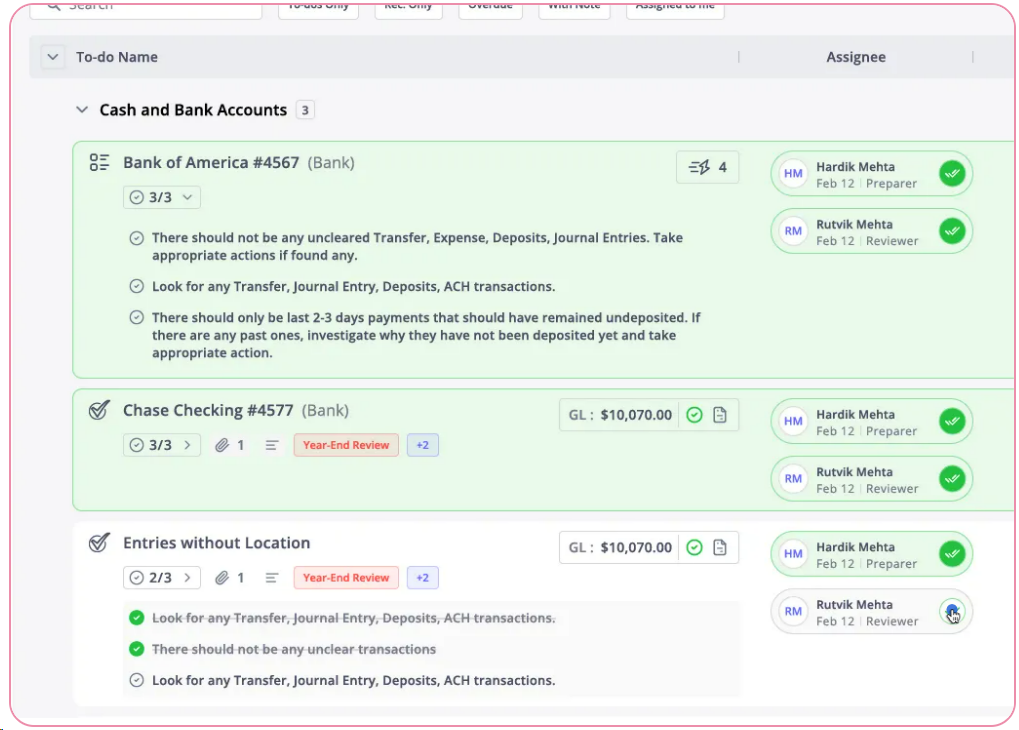

How Can Xenett Simplify Your Financial Management?

Let’s talk about Xenett, a powerful tool designed to make managing your business finances much easier.

What Features Does Xenett Offer?

Xenett provides several tools to help with your bookkeeping, tax preparation, and financial planning:

- Comprehensive Tools for Bookkeeping: Xenett helps you keep track of all your business transactions, making sure everything is recorded correctly.

- Tax Preparation: The software organizes your financial records to make tax time less stressful. It ensures you have all the information you need to file your taxes accurately.

- Financial Planning: Xenett offers tools to help you plan for the future. You can create budgets, forecast your finances, and set financial goals.

How Does Xenett Simplify Your Finances?

- Automates Tasks and Organizes Records:

Transactions by vendors on single screen

Xenett takes care of repetitive tasks like entering data and tracking expenses.

It organizes all your financial records in one place, so you don’t have to worry about losing important information.

- Generates Detailed Financial Reports:

With Xenett, you can easily generate detailed reports that show how your business is performing.

These reports include profit and loss statements, balance sheets, and cash flow statements.

They help you understand your business’s financial health at a glance.

Using technology like Xenett can save you time, reduce errors, and give you a clear picture of your business finances. This allows you to focus more on growing your business and less on managing your books.

Tip #3. Planning for Financial Success

Why Should You Develop a Budget?

So what about budgeting? Creating a budget is like drawing a roadmap for your business. It helps you plan where your money will go and how you will spend it.

What’s the Importance of Revenue Projections and Expense Tracking?

- Revenue Projections: These are estimates of how much money your business will make in the future. They help you set realistic financial goals.

- Expense Tracking: This means keeping track of all the money your business spends. It helps you avoid overspending and stay within your budget.

Statistics on Businesses with Excellent Financial Health and Budgeting Practices

Did you know that businesses with good budgeting practices are more successful? Studies show that over 60% of businesses with excellent financial health always create a budget. They also keep a separate bank account for payroll, which helps them manage their money better.

How Can Financial Projections Help Your Business?

- Planning for Growth: Knowing how much money you’ll make and spend helps you plan for future growth. You can decide when to hire more staff, buy new equipment, or expand your business.

- Securing Financing: Lenders and investors want to see financial projections before giving you money. It shows them that you’ve thought about the future and have a plan to repay loans or use investments wisely.

- Communication with Stakeholders: Sharing your financial projections with your team, partners, or investors helps everyone understand the business’s financial health and goals.

Tip #4 Keeping Accurate Records

What Records Should You Keep for Your Business?

Keeping good records is like keeping a diary of your business’s financial life. It helps you track everything and stay organized.

Why Is Accurate Record keeping Important?

- Tax Compliance: Good records make it easier to file taxes correctly and avoid penalties.

- Financial Health: Accurate records help you understand how your business is doing financially. You can make better decisions when you know exactly where your money is going.

Types of Records to Maintain:

- Gross Receipts: All the money your business makes from sales.

- Expenses: All the money your business spends to operate.

- Fixed Assets: Items like equipment or property that your business owns.

Use of Receipt Scanners and OCR Technology:

Using receipt scanners and Optical Character Recognition (OCR) technology can help you keep digital copies of your receipts. This makes it easier to track expenses and stay organized.

How Can Profit and Loss Statements Help You?

A Profit and Loss (P&L) statement is a report that shows how much money your business made and spent over a certain period.

What Information Should a P&L Statement Include?

- Gross Profit: Total sales minus the cost of goods sold.

- Net Profit: Gross profit minus all other expenses.

- Operating Profit: Profit from regular business operations.

- Profit Before Tax: Profit before deducting taxes.

A P&L statement gives you a clear snapshot of your business’s financial health, helping you make informed decisions.

Tip #5 Choosing the Right Accounting Methods

Which Accounting Method Should You Choose?

There are two main accounting methods: cash basis and accrual accounting.

The Difference Between Cash Basis and Accrual Accounting

- Cash Basis Accounting: You record income when you receive cash and expenses when you pay them. It’s simple and easy to manage.

- Accrual Accounting: You record income when you earn it and expenses when you incur them, regardless of when the cash is actually received or paid. It provides a more accurate picture of your business’s financial health.

Importance of Consistency and GAAP Requirements

Consistency in using the same accounting method helps you compare financial data over time. Generally Accepted Accounting Principles (GAAP) require accrual accounting for larger businesses, but small businesses can choose the method that works best for them.

How Can You Keep Your Books Up to Date?

Automating these tasks saves you time and reduces errors. It ensures that all transactions are recorded promptly.

Linking Bank Accounts with Accounting Software for Seamless Integration

Connecting your bank accounts to your accounting software helps you automatically import transactions. This keeps your books up to date without manual data entry.

Tip #6 Managing Your Expenses and Payments

How Can You Optimize Accounts Payable Terms and Invoicing?

Managing how and when you pay your bills and send invoices can help improve your cash flow.

How to Manage Cash Flow Efficiently?

- Strategic Payment Scheduling: Pay your bills on a schedule that maximizes your cash flow. For example, take advantage of credit terms offered by suppliers.

- Encouraging On-Time Payments from Customers: Offer discounts for early payments or run credit checks on new customers to ensure they can pay on time.

Why Should You Monitor High-Cost Expenses?

Keeping an eye on your biggest expenses helps you control costs and improve profitability.

How to Keep Track of Labor and Inventory Costs?

- Using Time-Tracking Software: Helps you understand labor costs by tracking the time employees spend on different tasks.

- Using Inventory Management Software: Helps you monitor inventory levels, track inventory turnover, and reduce losses from obsolete inventory.

Tip #7 Staying on Top of Tax Preparation

How Can You Remember and Stick to Tax Deadlines?

Meeting tax deadlines is crucial to avoid penalties.

Why Is It Important to Meet Tax Deadlines?

Late tax payments can result in fines and interest charges. Staying on top of deadlines helps you avoid these extra costs.

Tools for Setting Reminders and Organizing Tax-Related Tasks

Use calendar reminders, apps, or software to keep track of important tax dates and tasks.

Should You Seek Professional Tax Preparation Guidance?

What Are the Benefits of Hiring a Tax Professional?

- Accuracy: A tax professional can help ensure your taxes are filed correctly.

- Time-Saving: They handle the complex parts of tax preparation, saving you time.

- Deductibility of Tax Preparation Costs: For sole proprietors, the cost of hiring a tax professional can be deductible.

Tip #8 Continuous Learning and Improvement

Why Attend a Free HMRC Workshop?

HMRC (Her Majesty’s Revenue and Customs) offers workshops to help business owners understand tax requirements and financial management.

What Can You Learn from HMRC Workshops?

- VAT (Value Added Tax): How to manage VAT for your business.

- Setting Up a Limited Company: Steps and benefits of forming a limited company.

- Online Filing: How to file your taxes and other documents online.

Value of Continuous Education for Financial Management

Continuous learning helps you stay updated on the best practices for managing your business finances. It ensures you are well-prepared to handle any financial challenges that come your way.

Conclusion: Master Your Business Finances for Success

High five! 🖐️

You made it to the end.

We’ve covered a lot, so let’s quickly recap what we talked about:

- Why Proper Financial Management is Crucial: We discussed the importance of tracking cash flow, budgeting, tax compliance, and securing financing.

- Keeping Business and Personal Finances Separate: We learned how opening a business bank account can make expense tracking easier, provide personal liability protection, and help you access business credit.

- Leveraging Technology for Financial Success: We explored the benefits of accounting software and tools like Xenett to automate tasks, reduce errors, and generate detailed financial reports.

- Planning for Financial Success: We emphasized the importance of developing a budget, making revenue projections, and tracking expenses to ensure your business stays on the right path.

- Keeping Accurate Records: We highlighted the types of records you need to maintain and how tools like receipt scanners and OCR technology can help.

- Choosing the Right Accounting Methods: We explained the differences between cash basis and accrual accounting and the importance of consistency.

- Managing Your Expenses and Payments: We looked at strategies for optimizing accounts payable and invoicing, as well as monitoring high-cost expenses.

- Staying on Top of Tax Preparation: We discussed the importance of meeting tax deadlines and the benefits of hiring a tax professional.

- Continuous Learning and Improvement: We suggested attending free HMRC workshops and keeping up with financial management education.

While going through this guide, I’m sure you noticed how often I mentioned Xenett. So, do check out Xenett when you have a moment. It can simplify your financial management and save you a lot of time and effort.

Need more reasons to give it a try? Start with a free trial and see how it can transform your business finances. No credit card needed — just your email, and you're all set!

That’s all for today.

See you next time.

Happy managing till then!